1

PUBLIC

PUBLIC

TABLE OF CONTENTS

EFFECTIVEDATE.....................................................................................................................3

1.0 SUPERVISORY GUIDANCE NOTE ON THE USE OF THE GHANA CARD FOR

FINANCIAL TRANSACTIONS.......................................................................................4

2.0 VERIFICATION PROCEDURES FOR ON-BOARDING CUSTOMERS..........................4

3.0 VERIFICATION PROCEDURES FOR ON-BOARDING CUSTOMERS ON MOBILE

APPLICATIONS AND INTERNET BANKING PLATFORMS.........................................5

4.0 VERIFICATION PROCEDURES FOR EXISTING CUSTOMERS UNDERTAKING

TRANSACTIONS............................................................................................................5

5.0 VERIFICATION PROCEDURES FOR FOREIGN NON-RESIDENTS WHO ARE IN

THE COUNTRY FOR LESS THAN 90 DAYS AND UNDERTAKING ONE-OFF

TRANSACTIONS............................................................................................................6

6.0 VERIFICATION PROCEDURES FOR FOREIGN DIPLOMATS AND THEIR

DEPENDENTS ................................................................................................................6

7.0 VERIFICATION PROCEDURES FOR THIRD PARTIES AND NON-FACE-TO-FACE

TRANSACTIONS............................................................................................................7

8.0 NO MATCH OR FAILED VERIFICATION PROCEDURES ...........................................7

9.0 PROCEDURES FOR NO MATCH OR FAILED VERIFICATION OF EXISTING

CUSTOMERS..................................................................................................................8

10.0 PROCEDURES FOR FAILED AND NO MATCH VERIFICATION FOR ON-BOARDING

........................................................................................................................................8

11.0 PROCEDURES FOR “FAILED AND NO MATCH” VERIFICATION FOR THIRD

PARTY TRANSACTIONS...............................................................................................9

12.0 ESCALATION MATRIX FOR THE NIA VERIFICATION SYSTEM ..............................9

13.0 PERFORMING ONLINE VERIFICATIONS ...................................................................9

14.0 CAUSES AND SOLUTIONS TO FAILED FACE VERIFICATION RESULTS ...............10

15.0 CAUSES AND SOLUTIONS TO FAILED SINGLE FINGER VERIFICATION RESULT

......................................................................................................................................11

16.0 CAUSES AND SOLUTIONS TO FAILED NO CARD PRESENT VERIFICATION

RESULT........................................................................................................................12

17.0 CAUSES AND SOLUTIONS TO FAILED VERIFICATION RESULTS..........................13

18.0 STEPS FOR NOTIFICATION AND RECTIFICATION OF A “NO MATCH” OR

“FAILED” VERIFICATION..........................................................................................14

19.0 BUSINESS CONTINUITY PROCEDURES FOR THE USE OF THE GHANA CARD ....14

20.0 PROCESS FLOW ON HOW TO ACCESS VERIFICATION DATA ON THE MECO

DEVICE ........................................................................................................................15

21.0 OTHER BCP STEPS/ PROCEDURES FOR INSTITUTIONS TO FOLLOW..................15

3.

2

PUBLIC

PUBLIC

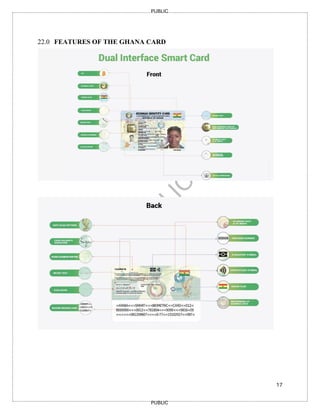

22.0 FEATURES OFTHE GHANA CARD............................................................................17

23.0 TRANSITIONAL PROVISIONS....................................................................................18

4.

3

PUBLIC

PUBLIC

EFFECTIVE DATE

This revisedSupervisory Guidance Note on the use of Ghana Card for Accountable Institutions,

October 2025 comes into effect from the date of issue and replaces the Supervisory Guidance Note

on the use of Ghana Card for Accountable Institutions, June 2022.

5.

4

PUBLIC

PUBLIC

1.0 SUPERVISORY GUIDANCENOTE ON THE USE OF THE GHANA CARD FOR

FINANCIAL TRANSACTIONS

The National Identity Register Regulations, 2012 (L.I. 2111) mandate the use of the

National Identity Card, commonly known as the “Ghana Card”, for transactions where

identification is required.

In furtherance of the above, the Bank of Ghana issued the Notice Number

BOG/GOV/SEC/01 mandating all Bank of Ghana licensed and regulated financial

institutions to accept the Ghana Card as the sole identity document for transactions.

This Guidance Note is to provide clarity to the Bank of Ghana Notice Number

BG/GOV/SEC/2025/36 issued 13th

November, 2025 and aims to ensure compliance with

Know Your Customer (KYC) and Customer Due Diligence (CDD) requirements.

2.0 VERIFICATION PROCEDURES FOR ON-BOARDING CUSTOMERS

1. Accountable Institutions (AIs) shall use only the Ghana Card to identify and verify all

customers, including Ghanaian Citizens living in Ghana and Abroad, Permanent

Residents and Economic Community of West African States (ECOWAS) Nationals who

are residents during onboarding (Account Opening)

2. AIs shall use only the Ghana Card to identify and verify Foreign Directors/Shareholders

and Non-Residents who are signatories to accounts during onboarding (Account

Opening).

3. AIs during the onboarding of new customers shall, in addition to KYC/CDD/EDD

requirements, apply the following:

a. Verify the identity of the customer using any of the biometric features the Ghana

Card, Non-Citizen Identity Card or Refugee Identity Card in the case of non-

Ghanaians.

b. Update customer KYC data set using information from the National Identity

Authority (NIA)

c. In cases where the following data sets acquired from NIA differ:

i. Secondary (Dynamic) data - The AIs shall verify and update using procedures

prescribed by the NIA in this Guideline. Such data set includes local phone

number, foreign phone number, residential address, postal address, digital-GPS

address, name of next of kin, address of next of kin, occupation and email

address.

ii. Primary data – The AIs shall refer the customer to NIA for updates regarding

their personal information. Such data set includes surname, first name, previous

names, date of birth, sex, height, picture and nationality.

6.

5

PUBLIC

PUBLIC

3.0 VERIFICATION PROCEDURESFOR ON-BOARDING CUSTOMERS ON

MOBILE APPLICATIONS AND INTERNET BANKING PLATFORMS

1. Given the inherent Money Laundering, Terrorist Financing and Proliferation Financing

(ML/TF/PF) risks associated with non-face-to-face technologies, identification and

verification shall not be risk-based.

2. AIs during the onboarding of new customers on mobile banking applications and

internet banking platforms shall conduct the following:

a. Verify the identity of the customer using the Ghana Card, Non-Citizen Identity

Card or Refugee Identity Card in the case of non-Ghanaians.

b. Utilise a liveness check to biometrically verify the customer.

c. Collect all KYC/CDD/EDD requirements as applicable in anti-money laundering,

combating the financing of terrorism and combating the financing of proliferation

of weapons of mass destruction (AML/CFT/CPF) laws, regulations and guidelines.

d. Update customer KYC data set using information from the National Identity

Authority (NIA).

e. In cases where the following data sets acquired from the NIA differ:

i. Secondary (Dynamic) data - The AIs shall verify and update using procedures

prescribed by the NIA in this Guideline. Such data set includes local phone

number, foreign phone number, residential address, postal address, digital-

GPS address, name of next of kin, address of next of kin, occupation and

email address.

ii. Primary data – The AIs shall refer the customer to NIA for updates regarding

their personal information. Such data set includes surname, first name,

previous names, date of birth, sex, height, picture and nationality.

4.0 VERIFICATION PROCEDURES FOR EXISTING CUSTOMERS UNDERTAKING

TRANSACTIONS

1. For existing customers in the following categories:

a) Ghanaian Citizens

b) Foreign National Permanently Resident in Ghana (e.g. ECOWAS Nationals)

c) Foreign National cumulatively resident in Ghana for at least 90 days

d) Dual Citizen

e) Foreign Directors/ Shareholders who are signatories to the account and operate the

account.

f) Refugees

2. AIs shall, on a risk-based approach, verify the identity of the customer

3. AIs as part of ongoing due diligence shall update existing customers' data.

4. In cases where the new data sets acquired from the NIA differ:

i. Secondary (Dynamic) data - The AIs shall verify and update using procedures

prescribed by the NIA in this Guideline. Such data set includes local phone

number, foreign phone number, residential address, postal address, digital-GPS

7.

6

PUBLIC

PUBLIC

address, name ofnext of kin, address of next of kin, occupation and email

address.

ii. Primary data – The AIs shall refer the customer to NIA for updates regarding

their personal information. Such data set includes surname, first name, previous

names, date of birth, sex, height, picture and nationality.

5. In the case where the customer does not physically possess the Ghana Card/ Non-Citizen

Identity Card/Refugee Identity Card, the AI shall use the biometric information to verify

and update appropriate customer records.

6. Where a customer has not registered for the Ghana Card, Non-Citizen Identity Card or

Refugee Identity Card, the AI shall not undertake any financial transaction for or on

behalf of the customer.

5.0 VERIFICATION PROCEDURES FOR FOREIGN NON-RESIDENTS WHO ARE

IN THE COUNTRY FOR LESS THAN 90 DAYS AND UNDERTAKING ONE-OFF

TRANSACTIONS

1. AIs shall only undertake the following one-off transactions for or on behalf of foreign

customers who are non-resident in the country:

a. Remittance;

b. Third-party deposit or withdrawal; and

c. ATM/POS (e.g. VISA/MasterCard) transactions.

2. AIs shall obtain and verify the identity of the customer using a valid international

passport.

3. AIs shall apply a risk-based approach in undertaking additional KYC/CDD/EDD

procedures at a minimum in obtaining the following:

a. visa information;

b. date of entry into the country;

c. foreign residential address; and

d. residential address in Ghana.

4. AIs shall keep records of the verification and transaction

6.0 VERIFICATION PROCEDURES FOR FOREIGN DIPLOMATS AND THEIR

DEPENDENTS

1. For all Foreign Diplomats and their Dependents undertaking the following transactions;

a. onboarding

b. one-off

c. on-going transactions.

2. AIs shall;

8.

7

PUBLIC

PUBLIC

a. obtain andverify the identity of the customer using an identity document such as

diplomatic passport/card issued by a competent authority

b. keep records of the verification and transaction.

c. in addition, apply a risk-based KYC/CDD/EDD procedure.

7.0 VERIFICATION PROCEDURES FOR THIRD PARTIES AND NON-FACE-TO-

FACE TRANSACTIONS

1. Given the inherent ML/TF/PF risks associated with third-party and non-face-to-face

transactions, identification and verification shall not be risk-based.

2. AIs in performing third-party transactions and in addition to KYC/CDD/EDD

requirements, shall conduct the following:

a. Verify the identity of the third-party using the Ghana Card, Non-Citizen Identity

Card or Refugee Identity Card in the case of non-Ghanaians.

b. Verify the biometrics of the third-party using finger (s) and/or face

3. In the case where a third party has been formally introduced by an introductory letter

from the account holder or a Board Resolution, the AI shall conduct the following:

a. Validate the introductory letter/board resolution

b. Verify the identity of the third-party using the Ghana Card, Non-Citizen Identity

Card or Refugee Identity Card in the case of non-Ghanaians,

c. Verify the biometrics of the third-party using finger(s) and/or face

d. Attach the third-party information to the account

4. AIs in performing multiple and/or linked transactions for third parties shall undertake

the following:

a. In the case where the third party is performing the transactions with the same

officers, the third party shall be verified once.

b. In the case where the third party is performing the transaction with multiple

officers, the third party shall be verified multiple times.

5. AIs in performing transactions of existing customers on mobile banking platforms shall

biometrically verify the identity using the finger (s) and/or face.

6. AIs shall keep records of the verification and transaction of both the third-party and non-

face-to-face transactions.

8.0 NO MATCH OR FAILED VERIFICATION PROCEDURES

8.1 NO MATCH

A “NO MATCH” verification is a case where:

1. The data (Card/Biometric) presented to the verification system does not match with

anyone in the system.

2. Only the biometric data presented for verification is successfully captured, but it does

not match the identity of a registered person.

9.

8

PUBLIC

PUBLIC

3. The GhanaCard PIN being used with the biometrics of the customer was mistyped.

4. The customer presenting the Ghana Card as identification and verification for

transaction(s) is not the lawful owner of the Ghana Card.

8.2 FAILED

A “FAILED” verification is a situation where;

1. the biometric data sent to the verification system is not of sufficient quality to be

processed.

2. there is poor network quality

9.0 PROCEDURES FOR NO MATCH OR FAILED VERIFICATION OF EXISTING

CUSTOMERS

1. Where there is “No Match” or “Failed” verification of identity for an existing

customer, the AI shall:

a. follow the escalation matrix for correction of the “No Match or “Failed” verification

as prescribed in the Identity Verification System Platform (IVSP) Support

Document, as indicated below.

b. contact the IVSP Customer Support Center for notification and rectification if the

escalation matrix procedure was unsuccessful.

c. apply a risk-based approach and use the unique verification code generated by the

National Identification Authority (NIA) for the identification of the customer.

d. advise the customer to contact NIA for an update of records.

10.0 PROCEDURES FOR FAILED AND NO MATCH VERIFICATION FOR ON-

BOARDING

1. Where this is a “No Match or Failed” verification of identity for a new customer, the

AI shall:

a. follow the escalation matrix for correction of the “No Match or “Failed” verification

as prescribed in the IVSP Support Document indicated below.

b. contact the IVSP Customer Support Center for notification and rectification if the

escalation matrix procedure was unsuccessful.

c. flag the account as post no debit

d. provide customer a ninety (90) days deferral period to update records before

completing the account opening process and making the account operational.

10.

9

PUBLIC

PUBLIC

11.0 PROCEDURES FOR“FAILED AND NO MATCH” VERIFICATION FOR THIRD

PARTY TRANSACTIONS

1. Where there is a “No match or failed” verification of identity for a third party, the AI

shall:

a. follow the escalation matrix for correction of the “No Match or “Failed” verification

as prescribed in the IVSP Support Document, as indicated below.

b. contact the IVSP Support Center for rectification and generation of a unique

verification code if the escalation matrix procedure was unsuccessful.

c. use the unique verification code generated by NIA for unsuccessful escalation

procedure for the identification of the customer in addition to KYC/CDD/EDD

procedures conducted.

12.0 ESCALATION MATRIX FOR THE NIA VERIFICATION SYSTEM

12.1 INTRODUCTION

This document highlights the techniques that can be used in cases of no match verifications.

The verification platform provides several methods to be used to verify Ghana cardholders.

In peculiar cases, the cardholder gets a “no match” result. If there is no doubt that the Ghana

cardholder is who they claim to be, AIs shall implement the following steps to resolve the

verification issues.

12.2 VERIFICATION METHODS

1. No Card Present or No Card PIN Verification: is used to verify a person who is

without the Ghana Card ID or does not know his / her Personal ID Number

(PIN). The verification is done using KYC or Yes/ No 4-4-2 device.

2. Single finger verification can be used to perform verifications. The preferred digits

are the thumbs or index fingers. If there is a “no match” result, the officer must

perform another verification with a different finger.

3. Face verifications can be performed. If this leads to a “no match” result, the teller

can verify using a single-finger verification.

4. Offline verification is also a method where the card is required

13.0 PERFORMING ONLINE VERIFICATIONS

13.1 HOW TO PERFORM YES/NO OR KYC FACE VERIFICATIONS CORRECTLY

1. To perform a Yes/No or KYC face verification, the end users' Ghana Card PIN and

biometrics are required.

11.

10

PUBLIC

PUBLIC

2. The administratorinputs the cardholder's Ghana Card PIN, selects the operation being

performed and takes the end user's photograph to receive the result. See the Online

verification user manual for detailed instructions.

14.0 CAUSES AND SOLUTIONS TO FAILED FACE VERIFICATION

RESULTS

Causes Solution

1. Poor room lighting

This is caused when the light in the room

is so dim that the image captured appears

dark and card holders’ features cannot be

read by the device.

1. Re-position the end user in a more lit-up

place

2. If 1 fails, perform finger verification

2. Glare

This is caused when the light reflects onto

the camera lens, so image captured is too

bright or has a light reflection on it and

makes the features difficult to read

1. Adjust the camera away from the light

glare

2. If 1 fails, perform finger verification

3. Smudges on the camera lens

This is caused when the camera lens is

dirty due to dust or fingermarks, so the

image captured appears blurry or not

clear

1. Periodically wipe the camera lens with a

clean cloth or tissue

2. Adjust the camera using the sides and

avoid holding the lens

3. If 1 fails, perform finger verification

4. Out of focus

This is caused when the image captured

did not focus on the subject i.e., the card

holder. This can be caused when the

subject fidgets while the image is being

captured. The image captured looks in

motion or blurred.

1. Request the card holder to look at the

camera until the image is captured

2. If 1 fails, perform finger verification

5. Wrong PIN

This is caused when an incorrect PIN is

entered during the verification i.e.,

numbers misplaced, more than 10 digits

etc. due to the embossment on the card or

faint digits

1. Look behind the card above the signature

on newer cards to locate the PIN

14.1 ALTERNATIVE SOLUTIONS TO FAILED FACE VERIFICATION

1. If the card is present, perform an offline verification using the handheld specialised

Android device (MECO)

12.

11

PUBLIC

PUBLIC

14.2 HOW TOPERFORM SINGLE FINGER YES/NO OR KYC

VERIFICATIONS CORRECTLY

1. To perform a Yes/No or KYC finger verification, the end user's Ghana card PIN and

biometrics are required.

The administrator inputs the Ghana Card PIN, from the dropdown lists selects the finger, selects

the mode of operation, and captures the finger initially selected from the dropdown list to complete

the verification process and receive a result. Refer to the Online verification user manual for

detailed instructions.

15.0 CAUSES AND SOLUTIONS TO FAILED SINGLE FINGER

VERIFICATION RESULT

Causes Solution

1. Placing the wrong finger on the scanner

This happens when the card holder puts

the wrong finger on the scanner. The

administrator selects which finger to scan,

if any other finger is placed on the scanner

the result will be a no match.

1. The administrator must make sure

that the card holder puts the correct

finger on the scanner.

2. If 1 fails, perform face verification

2. Faint fingerprints

This is caused when the card holders

prints are very faint due to dryness. The

print captured appears faint

1. The card holder must clean/ sanitize

their hands and ensure their hands are

dry before trying again.

2. Moisturize hands but ensure it is not

too greasy.

3. Apply pressure to the finger on the

reader

4. If all of the above fail, perform face

verification

3. Dirty fingerprint module

This is caused when the scanner surface

gets dirty from the accumulation of liquid

or dirt from people placing their fingers

on the sensor. This causes the sensor not to

read the finger properly.

1. check if the fingerprint module has

any liquid or dirt and clean it with a

clean cloth. If the dirt is sticking to

the module, gently clean it with wipes

or a damp cloth wetted with alcohol

(or a little water if there's no alcohol)

2. If 1 fails, perform face verification

4. Dirty fingers

This is caused when the card holder has

dirty, oily, or wet fingers. This causes the

sensor not to read the finger properly.

1. The card holder must clean/ sanitize

their hands and ensure their hands are

dry before trying again.

2. If 1 fails, perform face verification

5. Poorly placed fingers

This is caused when the card holder places

just the tip of the finger on the sensor. The

1. Place about 1/3 of the finger on the

reader

2. If 1 fails, perform face verification

13.

12

PUBLIC

PUBLIC

sensor is unableto capture the print

properly

6. Wrong PIN

This is caused when an incorrect PIN is

used during the verification i.e., numbers

misplaced, more than 10 digits etc. due to

the embossment on the card or faintly

printed digits

1. Look behind the card above signature

on the newer card to locate the PIN

15.1.1 ALTERNATIVE SOLUTIONS TO FAILED FINGER VERIFICATION

1. If the card is present, perform an offline verification using the MECO device.

15.2 HOW TO PERFORM NO CARD PRESENT (4-4-2) YES/NO OR KYC

FINGER VERIFICATIONS CORRECTLY

1. To perform a no-card Yes/No or KYC finger verification, the end users' 10

fingerprints shall be captured

16.0 CAUSES AND SOLUTIONS TO FAILED NO CARD PRESENT VERIFICATION

RESULT

Causes Solution

1. Faint fingerprints

This is caused when the card

holders prints are very faint due

to dryness. The print captured

appears faint

1. The card holder must clean/ sanitize

their hands and ensure their hands are

dry before trying again.

2. Moisturize hands but ensure it is not too

greasy.

3. Apply pressure to the finger on the

reader

2. Dirty fingerprint module

This is caused when the scanner

surface gets dirty from the

accumulation of liquid or dirt

from people placing their fingers

on the sensor. This causes the

sensor not to read the finger

properly.

1. check if the fingerprint module has any

liquid or dirt and clean it with a clean

cloth. If the dirt is sticking to the

module, gently clean it with wipes or a

damp cloth wetted with alcohol (or little

water if there's no alcohol)

3. Dirty fingers

This is caused when the card

holder has dirty, oily, or wet

fingers. This causes the sensor

not to read the finger properly.

1. The card holder must clean/ sanitize

their hands and ensure their hands are

dry before trying again.

14.

13

PUBLIC

PUBLIC

4. Poorly placedfingers

This is caused when the card

holder places just the tip of the

finger on the sensor. The sensor

is unable to capture the print

properly

1. Rest fingers on the reader so the base of

the fingers are not raised off it

2. Pay attention to the prompts given on

the screen and device so fingers are not

lifted before proper prints are captured

16.1 ALTERNATIVE SOLUTIONS TO FAILED NO CARD PRESENT

VERIFICATION

1. If the cardholder continues to receive a false verification and his/her card is present,

perform a KYC finger/face verification.

2. Should the above fail, perform an offline verification using the MECO device.

16.2 HOW TO PERFORM FACE VERIFICATIONS CORRECTLY

1. To perform a Yes/No or KYC face verification, the end users' Ghana card CAN

(Card Access Number) and biometrics are required.

2. The administrator shall input the cardholder's Card Access Number, which is the 6-

digit number beneath the picture on the Ghana Card and captures the end user's

image to complete the verification process and receive a result. Refer to the MECO

verification user manual for detailed instructions.

17.0 CAUSES AND SOLUTIONS TO FAILED VERIFICATION RESULTS

Causes Solution

1. Poor room lighting

This is caused when the light in the

room is dim so the image captured

appears dark and card holders’

features cannot read

1. Re-position in a more lit-up place and

redo

2. Perform finger verification

2. Smudges on the camera lens

This is caused when the camera

lens is dirty due to dust or finger

marks, so the image captured

appears blurry or not clear

1. Periodically wipe the camera lens

with a clean cloth or tissue

17.1 ALTERNATIVE SOLUTIONS

1. Perform a finger verification in offline mode using the MECO device.

15.

14

PUBLIC

PUBLIC

17.2 HOW TOPERFORM FINGER VERIFICATION IN OFFLINE MODE

USING THE MECO DEVICE

1. To perform a finger verification, the end user's Ghana card PIN and

biometric are required.

2. The administrator shall input the Cardholder's Card Access Number (CAN),

which is the 6-digit number beneath the picture on the Ghana Card, select

the finger and capture a fingerprint to complete the verification process and

receive a result. Refer to the Offline verification user manual for detailed

instructions

18.0 STEPS FOR NOTIFICATION AND RECTIFICATION OF A “NO MATCH” OR

“FAILED” VERIFICATION

1. The designated Officer shall follow the steps below if a “No Match” or “Failed”

Verification persists after adhering to the escalation matrix above:

a. Obtain the error code generated by the system

b. Send an email with the error code to the IVSP Support Channel at

https://verificationsupport.ims.gh.org/

19.0 BUSINESS CONTINUITY PROCEDURES FOR THE USE OF THE GHANA

CARD

1. AIs, in using the National Identification Authority’s Identity Verification System

Platform (IVSP) to perform verifications during system downtimes and updates shall;

a. Contact the IVSP Support Channel to ascertain that the system is down or

undergoing updates, if applicable.

b. Log the incident, indicating the time and date

c. Use the MECO device to conduct verification in offline mode by undertaking the

following:

Facial Verification

a) The physical Ghana Card of the customer shall be placed at the contact or

contactless reader points on the MECO device.

b) The administrator shall input the cardholder's Card Access Number (CAN), which

is the 6-digit number beneath the picture section of the Ghana Card and capture

the end user's live facial image to complete the verification process and receive a

result. Refer to the MECO verification user manual for detailed instructions.

Fingerprint Verification

16.

15

PUBLIC

PUBLIC

a) The physicalGhana Card of the customer shall be placed at the contact or contactless

reader points of the MECO device.

b) The administrator shall input the cardholder's Card Access Number (CAN), which is

the 6-digit number beneath the picture section on the Ghana Card and capture the end

users’ fingerprint to complete the verification process and receive a result. Refer to

the MECO verification user manual for detailed instructions.

3. In the case of no physical card present for third parties, only deposits shall be performed

and obtain details (Name, ID number, phone number, and signature at a minimum).

4. In the case of no physical card present for existing customers, only deposits shall be

performed and details obtained (name, ID number, phone number, and signature at a

minimum).

5. AIs shall keep records of the processes above.

20.0 PROCESS FLOW ON HOW TO ACCESS VERIFICATION DATA ON THE MECO

DEVICE

Institutions are required to configure a callback URL, which serves as the destination for receiving

verification result data. To access this data, users should consult their in-house technical team

responsible for the callback URL set up for assistance.

When the device operates in online mode (connected to a network), verification results are

automatically transmitted to the institution’s callback URL.

For offline mode (not connected to a network), the following steps must be followed to retrieve

the data:

▪ Open the control center on the MECO device and tap the Data/WIFI icon to connect the

device to a network. This action will send the data to the institution’s callback URL.

▪ Once connected, access the callback URL to view the verification data or response.

21.0 OTHER BCP STEPS/ PROCEDURES FOR INSTITUTIONS TO FOLLOW

Adoption of a multi-modal approach to verification is advised. This is to ensure alternative

verification solutions are readily available if challenges with a particular interface are being

faced.

a) In the event there is a challenge with capturing the fingerprint of a customer, the

institution shall proceed to conduct a facial verification on any of the verification

solutions that support facial verification.

17.

16

PUBLIC

PUBLIC

b) In theevent there is a challenge in capturing the facial biometrics of a customer, the

institution shall proceed to conduct fingerprint verification on any of the verification

solutions that support fingerprint verification.

To ensure better documentation and efficient tracking, institutions are now required to raise tickets

directly on the upgraded verification support portal at https://verificationsupport.imsgh.org/ This

portal enables seamless account creation, allowing the support team to quickly identify the

institution submitting the ticket.

▪ To sign in, navigate to the URL https://verificationsupport.imsgh.org/ and provide your full

name along with your corporate email address.

▪ You will receive an email from Verification Support - click the link within it to activate

your account.

▪ Next, create a secure password that adheres to the specified requirements. Your name will

be automatically pre-filled in the respective field.

▪ Once you have entered the required details, click the "Activate and Login" tab to complete

the process.

▪ Upon successful login, the user will be redirected to a dashboard where all features and

functionalities of the support platform are readily available.

18

PUBLIC

PUBLIC

23.0 TRANSITIONAL PROVISIONS

1.AIs shall note that linking one's Ghana Card to the bank account does not have an expiry

date and shall be part of ongoing KYC/CDD/EDD procedures.

2. Ghanaians abroad who do not have access to attain/acquire Ghana Card in their country of

residence should be allowed to use their passports to access banking transactions until such

time that the Ghana Card will be made available for them to attain/acquire.

3. Deposits (cash, cheque, transfers) by third parties into accounts of customers (account

holders) who have not updated their records with the Ghana Card should be allowed by

financial institutions. However, no debit withdrawal should be placed on such customer

accounts.

4. In line with the National Identity Registration Regulation L.I. 2111(2), which exempts

Diplomatic Corps from usage of the Ghana Card, members of the Diplomatic Corps should

be allowed to use the foreign passport as a means of identification for banking transactions.